An intergenerational perspective on TPD planning

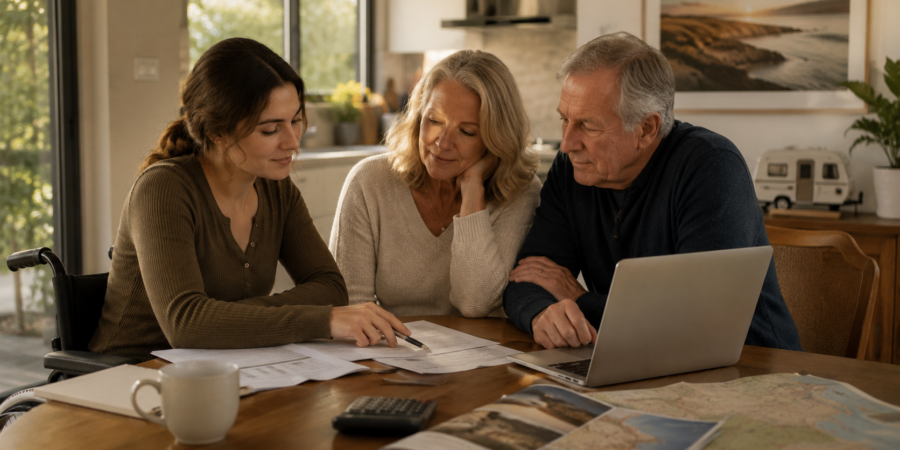

A TPD claim inside a family with a chronically ill adult child involves more than the insurance question.

- TPD cover lapsing does not necessarily extinguish a claim.

- Superannuation access under a TPD condition of release is a separate process from the insurance claim.

- Centrelink means testing can interact with superannuation access timing, and a poorly sequenced withdrawal may disrupt entitlements built up over years.

- Parents absorbing care costs informally may be heading toward a less secure retirement than they realise.

- An estate that distributes directly to a DSP beneficiary can disrupt their entitlements, but careful estate planning can help manage this.

- The superannuation strategy can affect the estate, the Centrelink position can affect the trust design, and looking at one without the other can produce the wrong outcome. This is exactly why intergenerational TPD planning treats these as one connected plan rather than six separate problems, and why a single professional may not be able to cover all of it alone.

Intergenerational TPD planning starts with a simple fact: a TPD claim rarely affects one person only. It means looking beyond the claim itself and considering how illness, disability, superannuation, Centrelink and estate planning affect the whole family.

Parents keep helping, retirement gets delayed, savings are used without a plan, and siblings may start wondering what will happen later.

Everyone may be trying to do the right thing, but without advice that connects the pieces, no one may be looking at the whole structure.

These situations can feel unique when a family is living through them, but they are far more common than people realise. The impact is emotional, practical and often deeply financial.

It can involve parents looking after adult children, adult children looking after parents, and families carrying care responsibilities while trying to protect retirement, housing, support payments and future inheritance.

Australia is moving through a major intergenerational wealth transfer, but the outcome is not shaped by family intention alone. Superannuation rules, Centrelink rules, tax, insurance contracts, estate planning and disability support can all influence who receives what, when, and with what consequences.

A family question, not just a claim question

I help moderate a Facebook group for people navigating TPD claims.

Recently, a mother posted on behalf of her 31 year old daughter, who was living with chronic illness and multiple diagnoses. She was asking whether a TPD insurance claim was worth pursuing, and whether accessing superannuation might be possible.

As the conversation developed, another issue emerged.

The mother mentioned that she and her husband had been hoping to retire. Supporting their daughter had made that feel difficult to achieve.

That is the critical point.

This was not only a question about whether the daughter might have a claim. It was also a question about long term support, informal care, parental retirement, Centrelink, tax, estate planning and whether the parents could still hold on to the life they had hoped to live.

It is the tension between devotion to someone you love and the quiet wish to still have a future of your own.

I consider that to be fundamentally a financial planning question. It requires different forms of professional advice sitting alongside each other, rather than being treated as separate and disconnected problems.

Super is not just an account

The first step is understanding the daughter’s superannuation history.

If her health condition developed while insurance cover was still active, a TPD insurance claim may still be worth exploring. Cover lapsing does not automatically mean the right to pursue a claim has disappeared. The timing of the illness or injury, the terms of the policy, the evidence and the history of cover all matter.

That is a different question from whether she can access her accumulated superannuation.

A TPD insurance claim and a TPD condition of release are related, but they are not the same thing. The insurance claim is assessed under the insurance contract. Access to accumulated superannuation is assessed under superannuation law and the fund’s requirements.

A person may be able to access accumulated superannuation even if the insurance outcome is uncertain, delayed, disputed or not available.

That can create options, but it can also create consequences. The question is not simply whether the money can be accessed. It is where the money should sit, when it should move, and what that movement does to tax, Centrelink and long term support.

Centrelink can change the strategy

Where a claim benefit or accumulated superannuation becomes available, it may be able to support the daughter’s financial position. But access needs to be considered carefully so it does not unnecessarily disrupt support payments.

The interaction between superannuation and means testing looks different at each life stage.

For example, superannuation in accumulation phase is generally not counted under the income and assets tests while a person is under Age Pension age, provided the fund is not paying them a superannuation pension. If the fund starts paying an income stream, that can be assessed differently.

That distinction can matter enormously for a person receiving the Disability Support Pension.

If the daughter is living with Mum and Dad, another practical question may arise. Is there a formal board and lodgings arrangement? If she is paying eligible accommodation costs and receives an eligible payment, Rent Assistance may be relevant, depending on her circumstances. Services Australia recognises board and lodging as a rent type for Rent Assistance, but eligibility depends on the details.

These are not side issues. They can be the difference between a family carrying everything informally and a family building a more sustainable support structure.

Mum and Dad’s retirement number may be wrong

Mum and Dad know they are supporting their daughter, but what they may not have measured is what that support is actually costing them against their own retirement plan. Those are two different problems.

The ASFA comfortable retirement benchmark for homeowners aged 65 and over currently sits at around $77,375 a year for a couple. That figure gives a useful guide to retirement spending, but it does not include the informal cost of supporting an adult child with chronic illness or disability.

It also does not capture the many informal costs that build over time, from extra groceries, utilities, transport and medical expenses through to lost work, delayed retirement, home modifications, unpaid care, emergency help and the quiet erosion of capital that can happen when support has no structure around it.

Add those costs in, and the number Mum and Dad actually need to retire on their own terms may be higher than the one they are planning around.

That gap matters when Age Pension entitlements become relevant. Structured well, Centrelink can become a genuine lever in the broader family plan. But it does not get pulled if nobody knows it is there.

Retirement travel, caravanning across the country, or simply having enough breathing room in later life may not be gone. But they may need to be planned for alongside the daughter’s long term support, not separately from it.

Two streams of advice: the core of intergenerational TPD planning

In a situation like this, there are usually two streams of advice: one for the daughter and one for Mum and Dad. Neither works properly in isolation.

For the daughter, the starting point is fund history. That tells us whether any TPD insurance cover existed, when it existed, what definitions applied and whether anything may be claimable.

If the claim is retrospective, medical evidence and legal advice may become important. The timing of diagnosis, symptoms, work capacity and cover history can all become relevant.

If the daughter meets a TPD condition of release, accumulated superannuation may become accessible regardless of the insurance outcome. The fund’s eligible service date also matters because it can affect tax on withdrawn amounts, now and in the future.

If she receives DSP, the next question is how any accessed money, income, support or accommodation arrangement may affect her Centrelink position.

For Mum and Dad, the starting point is their own cash flow, assets, retirement goals and the cost of support they are already providing. Then comes the Age Pension position, including how means testing may apply when it becomes relevant.

Early inheritance gifting may sit inside that picture, but it needs to be handled carefully. Services Australia may continue to assess gifts or transfers where assets are given away or transferred for less than market value.

Where the daughter has access to superannuation after meeting a TPD condition of release, there may also be strategic questions about whether she can contribute some funds back into superannuation, depending on the rules, caps, eligibility and her broader Centrelink position.

The point is not that there is one right answer, but that the family needs a coordinated plan.

Estate planning is where the structure has to survive

Estate planning is where the whole picture has to hold together.

A distribution from an estate can completely change a support arrangement for a vulnerable beneficiary. A well intended inheritance can affect Centrelink, housing security, care arrangements and family relationships.

If the daughter continues to live at home, what happens if Mum and Dad enter aged care?

What happens to the security of the home? Who makes decisions? How is money managed? What happens if there are siblings?

How the daughter receives any benefit matters. A direct inheritance, testamentary trust, protective trust or Special Disability Trust may each have a place, but they are not interchangeable.

A plan built around the daughter’s needs also has to consider expectations elsewhere in the family. If siblings are involved, that conversation belongs in the planning, not after the documents are signed.

Estate planning should provide a guide for executors and beneficiaries. It works best when it is built while everyone is still living and while the family still has choices.

Why sequencing matters in intergenerational TPD planning

The order of decisions matters.

A poorly timed withdrawal can disrupt a Centrelink position that took years to establish.

A Will that does not control how assets reach a vulnerable beneficiary can undo otherwise careful planning.

A gifting arrangement made without understanding the thresholds can affect pension eligibility at exactly the wrong time.

A TPD benefit paid without considering tax, Centrelink, family support and estate planning can solve one problem while creating several others.

Each system influences the others. The superannuation strategy affects the estate structure, the Centrelink position affects the trust design, the gifting strategy depends on the retirement plan, and the retirement plan depends on the real cost of care.

This sequencing is what makes intergenerational TPD planning work in practice, not just in theory.

Getting one part right while getting the others wrong can still produce a bad outcome.

Intergenerational TPD planning for the professionals in the room

If you are working with families navigating disability, chronic illness, TPD claims, Centrelink or intergenerational support, the structural planning should run together.

They should not be dealt with one after the other, only after the claim is paid, only after the Will is drafted, or only when Mum and Dad finally realise retirement is no longer working.

These conversations belong together because the family is already living them together. This is intergenerational TPD planning in practice: family needs and professional advice moving together, rather than being stacked one after another.

Supporting a family member through a TPD claim? Plan around the whole family.

HFI works with families, and with the lawyers and advisers supporting them, to bring TPD claims, Centrelink, superannuation and estate planning into one coordinated plan.

Book an Appointment Read: Post-TPD Advice GuideRelated reading

- Gifting and the Age Pension, Services Australia

- Board and lodging rent type for Rent Assistance, Services Australia

- Total and permanent disability (TPD) insurance, Moneysmart

- ASFA Retirement Standard, Association of Superannuation Funds of Australia

- HFI: Post-TPD Financial Advice (After Approval)

- HFI: Centrelink Preclusion Period: What It Means for Your Financial Future

Important information

This article is general information only and does not take into account your personal circumstances. It does not constitute personal financial or legal advice. Outcomes for TPD claims, superannuation access, Centrelink entitlements, estate planning and tax depend heavily on individual circumstances, policy wording and fund rules. Centrelink rules, thresholds, gifting limits and benchmark figures such as the ASFA Retirement Standard change over time. Verify current figures with Services Australia and the relevant superannuation fund before acting. HFI does not provide legal advice or tax agent services unless expressly stated. You should confirm legal and claim-related matters with your lawyer and tax consequences with a registered tax professional.

Health & Finance Integrated is a Corporate Authorised Representative of Able Financial Services, ABN 27 646 319 164, AFSL 530596, Shop 6, 23 Hassall St, Parramatta 2150 NSW.